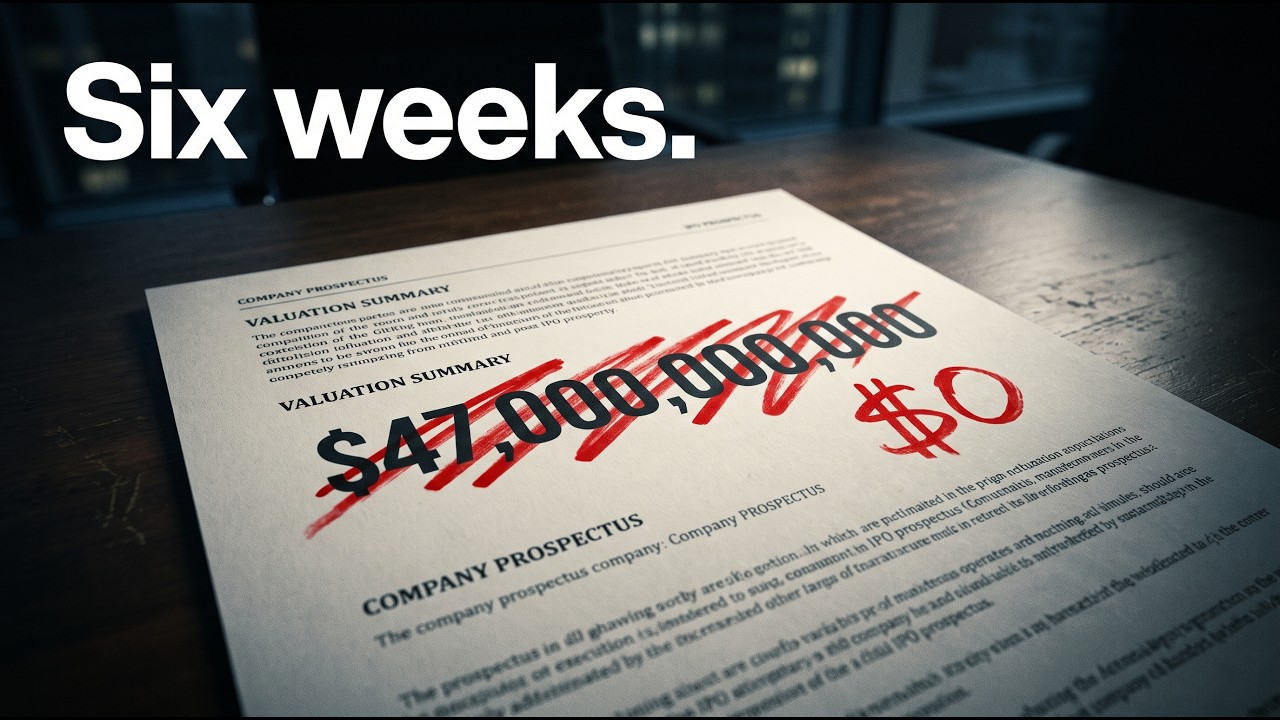

On August 14, 2019, WeWork was the most hyped startup in America: a $47 billion company preparing one of the most anticipated IPOs in tech history. Forty-two days later, the IPO was dead, the founder was out, and the company was weeks away from running out of cash.

No fraud trial. No hack. No market crash. All it took was a single public document.

Key Takeaways

- WeWork fell from a $47 billion valuation to a rescue at about $8 billion in roughly ten weeks in late 2019, undone by nothing more than its own IPO paperwork.

- The S-1 revealed a loss of more than $1.6 billion on about $1.8 billion of 2018 revenue: the company was losing roughly a dollar for every dollar it earned.

- SoftBank committed more than $18 billion to WeWork and ended with cumulative losses estimated around $16 billion by the 2023 bankruptcy.

- Adam Neumann exited with roughly $1.7 billion in total value while thousands of employees were laid off holding near-worthless stock options.

- WeWork filed for Chapter 11 in November 2023, four years after the failed IPO, and emerged in 2024 as a much smaller private company.

- Neumann failed upward: his next venture, Flow, raised $350 million from Andreessen Horowitz in 2022 and was later reportedly valued around $2.5 billion.

Why Was WeWork Ever Worth $47 Billion?

Because exactly one investor said it was: SoftBank set the $47 billion mark in a January 2019 funding round, and no public market ever validated the price.

Strip away the branding and WeWork was an office subletting business. It signed long leases on office buildings, chopped the space into desks, added beer taps and neon signs, and rented it out short-term. That model is over a century old, and it usually trades at real-estate multiples.

Adam Neumann sold something else entirely. WeWork wasn’t a landlord, he argued. It was a technology platform, a community, a movement to “elevate the world’s consciousness.” Growth was the only metric that mattered, and WeWork grew ferociously: founded in 2010 with a single SoHo location, it swelled into hundreds of locations across dozens of countries and became one of the largest private office tenants in cities like New York and London.

The pitch found its perfect buyer in SoftBank’s Masayoshi Son, who invested billions after a famously brief first tour of WeWork’s headquarters (reportedly around twelve minutes) and kept writing checks until SoftBank’s total commitment passed $18 billion.

“Who wins in a fight, the smart guy or the crazy guy?” Son reportedly asked Neumann, before telling him WeWork wasn’t being crazy enough.

Each SoftBank round marked the valuation higher, to $20 billion and then $47 billion, without a single public investor ever validating the price.

By 2019 the ambition had outgrown offices entirely. The company rebranded as The We Company, with arms for apartments (WeLive) and even an elementary school (WeGrow), while Neumann reportedly mused about becoming the world’s first trillionaire and living forever. None of it was hidden. That was the strange part: the excess was the brand.

What Did the S-1 Filing Actually Reveal?

That the most valuable startup in America was losing a dollar for every dollar it earned, and was governed like a family estate. The prospectus WeWork filed in August 2019 was supposed to be a victory lap. Instead, it read like a confession.

The red flags, in plain terms:

- A loss of more than $1.6 billion in 2018 on roughly $1.8 billion in revenue.

- “Community-adjusted EBITDA”: an invented profitability metric that stripped out basic costs and became an instant punchline on Wall Street.

- Self-dealing: Neumann personally owned stakes in buildings that he leased back to WeWork.

- The “We” trademark: Neumann had trademarked the word and charged his own company $5.9 million to use it, money he returned only after public outrage.

- Super-voting shares that gave him near-total control of a company he was treating like a family asset.

- Cash already extracted: Neumann had reportedly taken out more than $700 million through share sales and loans before the IPO even launched.

Analysts and journalists tore the document apart within days. The gap between the story and the business was no longer deniable. It is the same dynamic that has ended other over-leveraged empires, from Toys “R” Us to a long list of unicorns that never made it to the public markets.

Six Weeks of Freefall

| Date | Event |

|---|---|

| Aug 14, 2019 | S-1 prospectus goes public; scrutiny begins immediately |

| Early Sept 2019 | Reported IPO valuation slides from $47B toward $20B, then lower |

| Mid-Sept 2019 | WeWork postpones the IPO as demand evaporates |

| Sept 24, 2019 | Adam Neumann resigns as CEO under investor pressure |

| Sept 30, 2019 | The S-1 is withdrawn; the IPO is officially dead |

| Oct 22, 2019 | SoftBank’s rescue package values WeWork near $8 billion |

The terrifying part wasn’t just the valuation collapse. It was what the IPO’s failure revealed. WeWork had been burning cash so fast that it needed the offering’s proceeds, plus a linked multibillion-dollar credit facility that was contingent on the IPO raising billions, simply to keep operating. When the deal died, the company had months of runway left. SoftBank’s roughly $5 billion bailout wasn’t opportunism; it was life support.

The failure rippled far beyond one company. WeWork’s implosion helped slam the IPO window shut for money-losing unicorns, pushed SoftBank into damage control across its Vision Fund portfolio, and made “path to profitability” the phrase every startup suddenly rediscovered heading into 2020.

The $1.7 Billion Goodbye

The bailout’s most infamous feature was the exit package. To pry Neumann’s super-voting control away, SoftBank agreed to terms that gave the departing founder roughly $1.7 billion in total value, including hundreds of millions for his shares, a $185 million consulting and non-compete arrangement, a later settlement payment, and a massive credit line.

Meanwhile, thousands of WeWork employees were laid off in the months that followed (about 2,400 in the first wave alone), many holding stock options that were suddenly worth little or nothing. The man who built the bonfire was paid to walk away from it, a pattern of consequence-free failure at the top that echoes through stories like Elon Musk’s $44 billion Twitter deal.

The comparison that stings most is Theranos. Elizabeth Holmes went to prison because she lied to investors; she reported to federal custody in 2023. Neumann never needed to lie: everything scandalous about WeWork was disclosed, eventually, in its own offering document. Hype, it turns out, is legal.

The Critical Choice

The collapse was written years before the S-1. The critical choice belonged to Masayoshi Son: the decision to override doubt and fund Neumann’s vision at whatever valuation it took, beginning with a multibillion-dollar commitment made after a first meeting that reportedly lasted minutes.

That money did more than fuel growth. It manufactured the $47 billion number and removed every internal brake. Neumann’s excesses weren’t hidden from his biggest investor; they were bankrolled by him. Once the valuation was fiction, the only question was which document would expose it. The S-1 just happened to be the one that did. It’s the same lesson that runs through every entry in our collapses archive: the fatal decision usually comes at the peak, not the fall.

What Happened Next

WeWork limped on under SoftBank’s control for four more years, even completing a backdoor public listing through a SPAC merger in 2021 at about a $9 billion valuation whose shares then lost more than 99%, before filing for Chapter 11 bankruptcy in November 2023. By that point SoftBank’s cumulative losses on the company had reached an estimated $16 billion. WeWork emerged from bankruptcy in 2024 as a much smaller private company, running a fraction of its former locations under new ownership; Neumann himself reportedly tried to buy it back and was rebuffed.

Adam Neumann, meanwhile, raised hundreds of millions from Andreessen Horowitz for Flow, a residential real-estate startup valued around $2.5 billion. In Silicon Valley, the punishment for losing other people’s billions is, apparently, a fresh check.