Three companies make roughly 95% of the world’s DRAM, the memory inside every PC, phone, server, and games console on Earth. One of them once paid a $300 million criminal fine for fixing the price of that memory. And in 2026, RAM prices are surging faster than at any point in a generation.

This time, nobody needs a secret meeting.

Key Takeaways

- Three companies control roughly 95% of global DRAM: Samsung, SK Hynix and Micron, the survivors of a field that held more than 20 manufacturers in the mid-1990s.

- The industry has a criminal record: for fixing prices between 1999 and 2002, Samsung paid a $300 million US fine, Hynix $185 million, Infineon $160 million and Elpida $84 million.

- Micron confessed first and paid nothing: it cooperated under the DOJ’s leniency program and escaped US criminal fines entirely.

- Executives went to prison: multiple memory-industry managers served US jail terms over the conspiracy.

- Early-2026 forecasts projected DRAM contract prices jumping around 63% in a single quarter, with NAND flash rising by as much as 75%.

- Relief may not arrive before 2028: the manufacturers themselves have warned that AI-driven shortages could persist for years.

How Did the Memory Market Shrink to Three Companies?

Through three decades of brutal boom-bust cycles that bankrupted or absorbed everyone else, more than 20 DRAM makers in the mid-1990s became exactly three. Samsung Electronics, SK Hynix, and Micron Technology now sit at the top of one of the most concentrated markets in the global economy.

The consolidation reads like a casualty list:

- 1998: Texas Instruments quits, selling its memory operations to Micron

- 1999: NEC and Hitachi fold their DRAM units into Elpida, Japan’s consolidated champion

- 2009: Qimonda, Infineon’s spun-off memory arm, goes bankrupt in the financial crisis

- 2012-2013: Elpida collapses into bankruptcy; Micron buys it for about $2.5 billion

- Today: three firms hold roughly 95%, with Taiwan’s Nanya and a few others sharing scraps

The brutality is foundational. Memory is the business Intel itself famously abandoned in 1985 under withering Japanese price competition, a retreat so painful it became Silicon Valley strategy folklore. Every downturn since has washed more players out, and each survivor emerged with a bigger slice of the market.

That structure matters because memory is a commodity. One stick of DDR5 is functionally interchangeable with another, so in a healthy market, competition should grind margins toward zero. Instead, the industry moves with eerie synchronization: production cuts arrive together, supply stays tight together, and prices rise together.

Economists call it a tight oligopoly. PC builders call it something less polite.

What Actually Happened in the DRAM Price-Fixing Scandal?

Between 1999 and 2002, the world’s memory makers coordinated the prices they charged major PC builders, and the US Department of Justice proved it, extracting guilty pleas and more than $700 million in criminal fines.

The suspicion was never paranoia. It’s precedent. In 2002, the DOJ opened a Sherman Act investigation into DRAM manufacturers after memory prices spiked while PC makers like Dell and HP screamed about collusion. The investigation confirmed it, and the guilty pleas came in waves.

| Who | Year | Penalty |

|---|---|---|

| Infineon Technologies | 2004 | $160 million US criminal fine |

| Hynix Semiconductor | 2005 | $185 million US criminal fine |

| Samsung Electronics | 2005 | $300 million US criminal fine |

| Elpida Memory | 2006 | $84 million US criminal fine |

| Multiple memory makers | 2010 | Over €331 million in EU fines |

Samsung’s $300 million penalty was at the time one of the largest criminal antitrust fines in US history, and several executives served prison sentences. Yet against the tens of billions in annual revenue flowing through the memory market, the fines registered as a rounding error: a cost of doing business, paid years after the profits were banked.

The most revealing name is the one missing from the table: Micron. It cooperated with investigators under the DOJ’s corporate leniency program and escaped US criminal fines entirely, the classic prisoner’s-dilemma defection that antitrust enforcement is designed to reward.

Accusations didn’t stop there. A US class action filed in 2018 alleged the big three had coordinated supply cuts in 2016-2017 to inflate prices again; that case was ultimately dismissed, and the dismissal survived appeal: proof of how hard parallel behavior is to prosecute when three firms can read each other’s public signals perfectly. China’s price regulator opened its own investigation into all three companies in 2018 after memory prices had roughly doubled; no public penalty ever followed.

Why Are RAM Prices Exploding in 2026?

Because AI data centers are consuming the world’s memory supply, and the big three have shifted fabrication capacity toward high-margin AI chips instead of ordinary consumer DRAM.

Training and running large AI models requires staggering quantities of memory, especially HBM, the high-bandwidth DRAM stacked next to Nvidia’s accelerators, which has reportedly been sold out far in advance. As data centers absorbed the industry’s output, manufacturers shifted capacity away from ordinary consumer DRAM toward premium AI chips, the same demand wave that reshaped the processor world when Nvidia lapped Intel.

The result hit consumers in 2025 and got worse in 2026. Market forecasts in early 2026 projected DRAM contract prices jumping around 63% in the second quarter alone, with NAND flash rising by as much as 75%. Samsung and SK Hynix publicly warned that AI-driven shortages could stretch to 2027 and beyond.

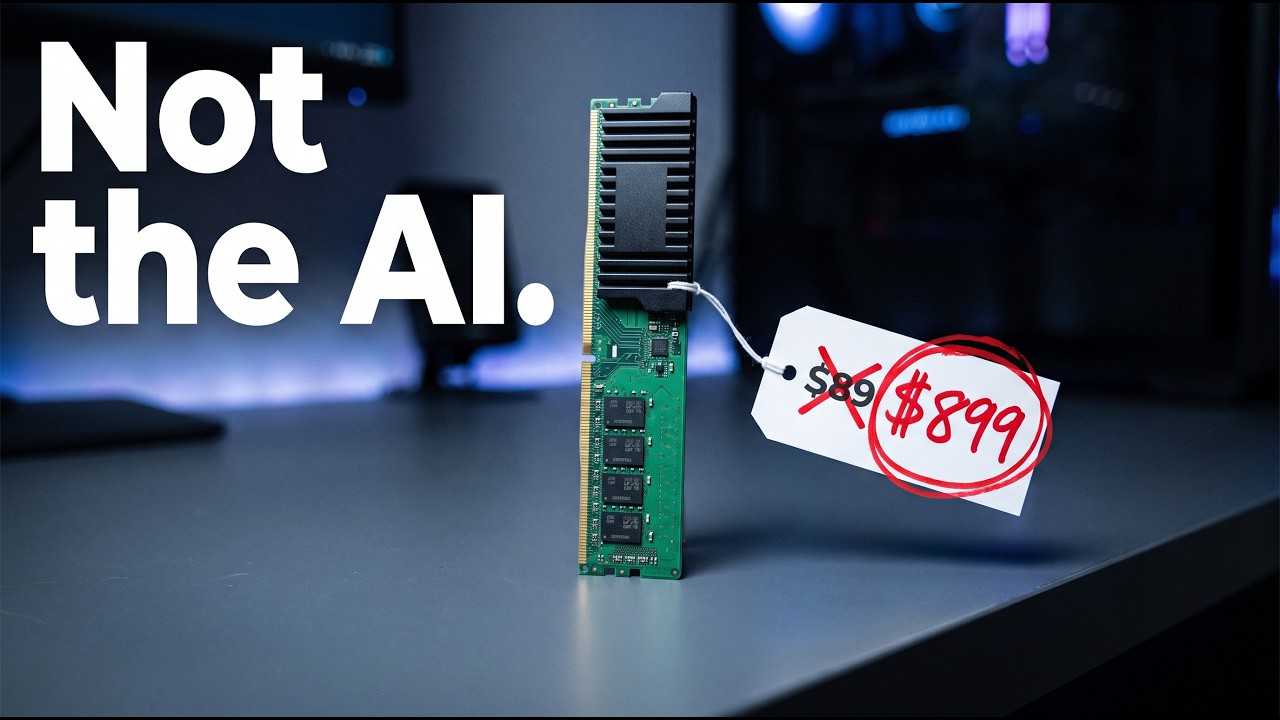

For anyone building a PC, the effect is simple: the RAM kit that cost $90 two years ago now costs multiples of that, if it’s in stock at all. The squeeze lands on everyone downstream, from budget builders priced out by the phase-out of older DDR4 stock to the gaming industry whose consoles and GPUs are built around the same silicon.

Why Regulators Can’t Touch It

Here’s the uncomfortable truth: what’s happening now is probably legal. Explicit price fixing (phone calls, emails, agreements) is a crime. But “conscious parallelism,” where three firms independently decide that restraint is more profitable than competition, is not.

With only three players, no secret cartel is required. Each company announces capacity plans, earnings, and “supply discipline” in public. Each can see that flooding the market would crater prices for everyone. The 2002-era conspirators needed covert coordination; their successors need only quarterly earnings calls. It’s a structural problem regulators across big tech keep running into: the law punishes the conspiracy, not the concentration that makes conspiracy unnecessary.

The Critical Choice

The decision that made 2026’s price shock inevitable wasn’t made in 2026. It was made across two decades of merger approvals and slap-on-the-wrist settlements. Regulators proved they could catch and fine a memory cartel, then allowed the market to consolidate until only three firms remained standing.

Once the survivors’ market share hit 95%, collusion became obsolete. The 2005 fines punished the crime while preserving the structure that produced it, and a market structure is far more durable than any conspiracy. Every price spike since has been the compound interest on that choice, paid by everyone who buys electronics and collected by three companies with money and power that most governments can only envy.

Where Things Stand Now

As of mid-2026, relief is nowhere in sight. AI data center construction keeps accelerating, HBM capacity is sold out far in advance, and the big three have little incentive to over-build ordinary DRAM capacity that would crash prices later. Executives have floated the possibility of shortages persisting toward 2028.

The wild card is China. State-backed ChangXin Memory Technologies (CXMT) has been scaling up DRAM output and, by most estimates, holds a single-digit share concentrated in older, cheaper chips. But a genuine fourth player would change the arithmetic, which is exactly why the incumbents and their governments watch it so closely.

New fabs are coming in the US, Korea, and Japan, but memory plants take years and tens of billions of dollars to build. Until that capacity lands, the world’s most important commodity chip remains what it has been for twenty years: a product three companies make, and no one truly competes to sell.